03-01-2007, 14:40

03-01-2007, 14:40

|

#1

|

|

TBB Family

Registriert seit: Apr 2002

Beiträge: 13.479

|

Fortune -- Die 10 besten USA Unternehmen für 2007

Fortune -- Die 10 besten Aktien für 2007

American International Group (AIG)

Hear the letters A-I-G, and chances are you think of the company's cantankerous former chairman and CEO, Maurice "Hank" Greenberg. During his four-decade reign the hard-charging Greenberg built AIG into the world's largest insurer, with operations in more than 100 countries. Investors loved him for his ability to somehow magically deliver 15 percent earnings growth quarter after quarter, and they awarded AIG shares a premium price/earnings multiple in the stock market.

The praise was overdone, of course, as the company got swept up in a series of highly publicized accounting scandals and government investigations that eventually cost Greenberg his job. In March 2005, Greenberg and several top executives resigned, leaving others to mop up the mess.

Nearly two years later, however, it's clear that AIG was no Enron. Under CEO Martin Sullivan, a 30-year company veteran, AIG has survived restating five years' worth of earnings, has paid billions to settle fraud charges with government authorities, and is reporting impressive profit growth once again. Led by a strong showing in its property and casualty business, the company registered a 38 percent jump in net income in the first three quarters of 2006 before investment gains or losses, to $11.6 billion. As Don Yacktman, who recently purchased more than 100,000 shares for his Yacktman Funds, puts it, "A little bit of plastic surgery and - voilà! - the ugly duckling becomes a swan."

Expect more strong results in 2007. Hurricane Katrina, which damaged billions of dollars' worth of homes, commercial structures and energy facilities, should help AIG's P&C business, which accounts for 33 percent of profits, because it allowed the company to boost premiums and impose more stringent terms and conditions on commercial policies. Meanwhile, AIG's foreign life-insurance unit, which accounts for 28 percent of earnings, should continue its rapid expansion, particularly in the immense Asian market.

Wall Street analysts have constructed fancy models to try to figure out how much of a premium AIG shares should fetch in the post-Greenberg era, if any. But their numbers are at best educated guesses. What's clear is that the stock is cheap, trading for 12 times estimated 2007 earnings, close to its historical low. And growth prospects are attractive, with profits projected to increase 13 percent annually for the next few years.

Altria (MO)

We've been recommending Altria Group for the past several years, and the stock has consistently been one of our best performers. We're picking it again for 2007. With about $100 billion in sales, the company - love it or hate it - is the world's largest cigarette maker and, through its Kraft Foods subsidiary, one of the biggest food processors. In the U.S., Marlboro, the top-selling cigarette brand, continues to thrive by stealing share; it now controls 41 percent of the market. Overseas sales are growing rapidly. The company now accounts for 60 percent of cigarette sales in Mexico, nearly 40 percent in Western Europe and 25 percent in Japan.

The litigation picture continues to improve, making costs far more predictable. In August a federal judge overseeing the government's landmark tobacco lawsuit ruled that she didn't have the authority to order major financial remedies, including industry-funded smoking-cessation programs. In November the Supreme Court refused to revive a $10 billion award against Altria's Philip Morris USA related to the marketing of "light" cigarettes.

Finally, there's the likely spinoff of Kraft Foods, a move that investors have long believed would unlock further value for Altria shares. "That's the key reason we're holding it," says David Dreman of Dreman Value Management, which owns 17 million shares. "As long as the companies are together, you won't get the full value for Philip Morris." The precise timing of the sale is to be announced at the company's Jan. 31 board meeting. In the meantime, Altria is selling for 15 times projected 2007 earnings and offers a fat 4.1 percent dividend yield.

ConocoPhillips (COP)

With oil and natural-gas prices easing from their 2006 peaks, buying into a big energy company might seem dangerous. But barring an unforeseen collapse in commodity prices, ConocoPhillips should turn in a solid performance.

Formed by the 2002 merger of midsized oil firms Conoco and Phillips Petroleum, the Houston energy company is the third-largest U.S. oil operator, behind Exxon Mobil and Chevron. With total U.S. refining capacity of 2.2 million barrels a day, it's the nation's second-largest refiner after Valero. And thanks to its recent $35 billion purchase of Burlington Resources, ConocoPhillips is the country's largest natural-gas producer. This diverse business mix helps smooth earnings.

Unlike many oil industry executives, CEO Jim Mulva isn't sitting on the piles of cash he's built up over the past few years from high energy prices. Instead he's aggressively reshaping the company to spur growth. Mulva will spend $13 billion in 2007 to finance new drilling projects and upgrade investment-starved refineries. He also plans to reduce debt, repurchase stock and increase the dividend; the current yield is 2.1 percent.

What's perhaps most attractive about Conoco is the stock price. Shares sell for just seven times estimated 2007 earnings, a steep discount compared with Exxon Mobil and Chevron, which trade for 11 and nine times earnings, respectively. The gap stems largely from Mulva's willingness to embrace new projects and Conoco's relatively heavy (for an oil giant) debt load. But at 25 percent of capital, the debt is manageable, given Conoco's strong cash flows. And Mulva has proved a good steward of shareholder money. "The company does a great job getting the most out of its assets," says Morningstar analyst Justin Perucki.

Diamond Offshore (DO)

It's not often that you find stock investors and commodities traders betting on completely different economic outcomes. But that's exactly the disconnect that exists today with oil. Consider contract oil drillers like Diamond Offshore, Ensco, and Noble - vendors that hire out their drilling rigs to the likes of Chevron and Exxon Mobil for a daily fee. The rise in oil prices over the past few years has caused the day rates they charge for their rigs to skyrocket along with their share prices. Analysts expect Diamond's earnings to rise 178 percent in 2006, and since most of its rigs are already under contract at even higher rates for next year, analysts are expecting earnings to jump another 86 percent in 2007. "We're booking rigs out into '08, '09 and even 2012 at very high rates," says Diamond Offshore president Larry Dickerson, who notes that such contracts are rarely broken. "I'm not sure the stock market appreciates the strength of earnings that are going to come in '08 and '09."

Since May the stock market has essentially been betting that drillers' earnings would fall with the price of oil, now about $63 a barrel. How else to explain stocks with triple-digit earnings growth trading at single-digit P/E ratios? Yet whereas equity investors may think oil is headed lower, commodities traders - folks who presumably have a better feel for oil's fundamentals than the typical stock jockey - are wagering the other way. The price of December 2007 oil futures is now near $70 a barrel, well above the current spot price.

Bob Rodriguez, manager of the FPA Capital fund, considers drillers a rare pocket of value in an otherwise overpriced market. Rodriguez, whose total returns rank him tenth among all equity-fund managers over the past 15 years, now has 40 percent of his fund in cash and 14 percent in oil drillers - most of which are down 20 to 30 percent from their May 2006 highs. "It doesn't surprise me that you've seen this rapid swing from superbullish to superbearish [on oil stocks]," says Rodriguez. "Most investors are rank speculators."

Available drilling rigs, particularly deep-sea drilling rigs, are in such short supply right now that the rates for rigs not yet under contract for 2007 are going through the roof, says A.G. Edwards oil-services analyst Poe Fratt. That's a rich opportunity for Diamond, which has more rigs available than most of its rivals. And it's one reason Diamond is Fratt's favorite driller.

Another: The company paid out a $1.50-a-share special dividend (on top of the regular 50-cent dividend) last February, and Fratt thinks 2007's special dividend - Dickerson confirms that there'll be one - could be anywhere from $3 to $5 a share. Add it up, and you've got a stock with that 86 percent projected earnings growth trading at only nine times next year's estimated earnings and offering a possible dividend yield of 5 percent to 7 percent. In other words, a steal.

General Dynamics (GD)

The biggest untold story out of Washington these days is the tremendous growth in federal tax revenues, which increased 12 percent in the fiscal year ended in September and 15 percent in 2005. David E. Baker, a defense analyst with Stanford Washington Research, thinks that a fast withdrawal from Iraq is unlikely, and that military and homeland-security spending will grow at least as much under a Democratic Congress as they did under the Republicans. Baker, a retired Air Force brigadier general, says Democrats understand that any effort to slow the growth of defense spending now would just become campaign fodder for Republicans seeking to portray them as soft on terrorism. "That's a label they want to avoid at all costs," he says.

Here's another reason to play defense: "Solid economic growth and the surge in global commodity prices have provided the liquidity necessary for a number of countries to fund arms buildups," Merrill Lynch chief investment strategist Richard Bernstein wrote in a recent report. Over the past several months the Pentagon has announced plans to sell $450 million in Northrop Grumman communications equipment to Jordan, $2.9 billion in General Dynamics Abrams tanks to Saudi Arabia, and $144 million in Lockheed Martin-made Patriot missiles to Japan.

The quick and easy way to play defense stocks is with the PowerShares Aerospace & Defense Portfolio (PPA), an exchange-traded sector fund. Our favorite individual stock: General Dynamics, which trades at 16 times 2007 earnings. Analysts expect those earnings to come in 13 percent ahead of this year's, and previous estimates have tended to be low.

Baker says the case for General Dynamics is straightforward: Democrats' defense budgets are likely to tilt toward spending "that directly supports the troops" - as opposed to futuristic projects like missile defense. Nicholas Chabraja, General Dynamics' CEO, agrees, to an extent, though he believes the issue transcends politics. "When troops get deployed in significant numbers it's not very surprising that the balance shifts toward supplying the current forces," Chabraja told Fortune in a rare interview. And as the leading manufacturer of tanks and armored vehicles, General Dynamics excels at supplying current forces.

Another reason to favor General Dynamics is its fast-growing corporate-jet business, Gulfstream, which is in itself a backdoor homeland-security play. With more and more corporations seeking to shield their executives from the hassles of flying commercial, Gulfstream now boasts an order backlog of $6.5 billion, up from $5.2 billion a year ago.

Quelle: CNN.com

__________________

liebe Grüße von Coco

|

|

|

|

03-01-2007, 14:44

|

#2

|

|

TBB Family

Registriert seit: Apr 2002

Beiträge: 13.479

|

Joy Global (JOYG)

Joy Global makes equipment for the mining industry, coal mining in particular. When commodity prices were soaring, so were Joy's shares - from $5 in January 2003 to $70 last April. But when prices began to fall, investors fled. As with many selloffs, this one was grossly overdone. Even with coal and copper prices now 25 percent off their midyear highs, analysts still expect Joy's earnings to grow 22 percent next year. "Yes, the price of coal has taken it on the chin," says portfolio manager and Joy fan John Buckingham of the Al Frank fund. "But the dropoff in its business didn't justify the huge decline in the stock price." As a result of the decline, the stock looks cheap - trading at a modest 15 times 2007 earnings.

CEO John Nils Hanson says Joy Global's earnings aren't nearly as sensitive to swings in coal and copper prices as Wall Street seems to believe. His customers don't decide to buy drills and electric mining shovels based on a six-month rise or fall in prices. "A copper mine can be a 40- or 50-year investment," he says.

Hanson considers China to be Joy's most promising market. China produces about two billion tons of coal annually, double the U.S. output, and the Energy Information Administration predicts China's demand for coal will triple by 2030. Roughly half of China's coal is mined without mechanized equipment (i.e., by hand, with picks and shovels). Joy expects revenue from China to hit $500 million by 2010, up from $200 million last year.

Microsoft (MSFT)

Tech junkies and media sophisticates love to blast Microsoft as an ailing dinosaur that's stuck in the pre-Internet era of the desktop PC. But shares of the software giant have been attracting an unlikely collection of exceptional investors. One is value veteran Marty Whitman at Third Avenue Funds, who purchased two million shares earlier this year, noting that the stock was selling for less than 15 times earnings (after deducting its cash holdings from the market value). On the growth side are the talented managers at the Jensen Fund, who also purchased a large position recently. Co-manager Bob Millen says Microsoft has everything Jensen's managers look for in an investment: high return on equity, robust earnings growth, growing free cash flows, and formidable competitive advantages.

Microsoft is launching the broadest barrage of new products in its 30-year history. In November it released Vista, the new version of the Windows operating system, and Office 2007, an upgrade of the popular software suite. Both businesses average operating margins of more than 70 percent, and they generate about 80 percent of Microsoft's total profits. And with Windows running on more than nine out of every ten computers in the world, the market is enormous. Other new products: everything from business servers to the new Xbox videogame machine.

After several stumbles, there's also evidence that Microsoft is getting Internet religion. In October the company struck a deal with Novell, a longtime enemy that is now a proponent of Linux, the open-source operating system that competes with Windows. The agreement makes it easier for customers to use both Windows and Linux software alongside each other on big computers, essentially brokering a peace between two opposing camps in the software industry.

Don Yacktman, another recent buyer, points out that the company has returned more than $90 billion to shareholders in stock buybacks and dividends over the past few years, a trend he says will continue. Says Yacktman: "Despite selling at one of the lowest price/earnings multiples in our portfolio, Microsoft possesses potentially the strongest platform for growth of any company we own."

J.P. Morgan Chase (JPM)

When J.P. Morgan Chase purchased Bank One in 2004, it also acquired the considerable management talents of that company's CEO, Jamie Dimon, who had turned around what was arguably the worst-run big bank in the country. Since taking the helm at J.P. Morgan, the brash Queens native has largely followed the same playbook he used at Bank One - installing new managers, meshing computer systems, and axing pricey outsourcing contracts. His efforts are paying off. Led by its robust investment-banking and wealth-management arms, the company is expected to report a 25 percent jump in earnings in 2006.

There's more upside to the turnaround. Chris Davis, who owns 72 million shares at Davis Funds, points out that the company is made up of a collection of businesses that can grow faster than the global economy and have room to improve both market share and profit margins. A quick way to look at the potential is to compare the return on equity - a key measure of profitability - of J.P. Morgan Chase and Citigroup. In 2005, Citigroup's ROE was 17.5 percent while J.P. Morgan's was 10.5 percent. To Davis, the gap means that J.P. Morgan Chase has "significant potential" to boost its profits.

The stock sells for 12 times projected 2007 earnings, roughly in line with industry rivals Citigroup and Bank of America; it yields 2.9 percent. Assuming 10 percent annual revenue growth over the next several years and continued savings from the merger, Morningstar analyst Craig Woker figures shares are worth $61.

RadioShack (RSH)

We know, we know. What the heck is a dog of a stock like RadioShack doing among Fortune's top picks? We had our doubts too when Bob Olstein - a fund manager obsessed with quality of earnings and good corporate governance - touted RadioShack as his favorite stock for 2007. "The next J.C. Penney," he called it. Not unlike Penney in the late 1990s, RadioShack has been a basket case of late, doing little to update its stores even as it lost market share to Best Buy and other retail rivals. RadioShack's earnings have been cut in half since 2000, and its stock price has shrunk 75 percent. To top it all off, CEO David Edmondson was forced to resign last February after it was revealed that he had fabricated parts of his résumé. The failure to vet Edmondson's credentials was a huge embarrassment for RadioShack's directors, but they redeemed themselves in choosing his replacement, retail industry veteran Julian Day. Kmart's CEO during its turnaround, Day came onboard in July, and Olstein - whose Olstein Funds owns 1 percent of RadioShack - sees early signs of progress, noting that debt, inventories and accounts receivable are all coming down.

Given Day's reputation as a shrewd cost cutter - at Kmart he turned a $5 million quarterly loss into a $155 million profit in one year - Olstein believes RadioShack can grow earnings from a projected 73 cents a share this year to $2 or more by 2008 or 2009. Apply a market multiple to $2 a share in earnings, and you get $35 - double the current stock price. And RadioShack is the kind of fixer-upper private-equity firms love to buy.

Day hasn't said much publicly about his plans, but Kaufman Brothers analyst SooAnn Roberts says that beyond closing less profitable stores and trimming payroll, it's clear what RadioShack needs to do: reduce the clutter, improve customer service, and scrap oddball electronics like metal detectors and CB radios to create more shelf space for what's hot. Roberts thinks the turnaround is doable, although she's the only analyst who rates RadioShack a buy. As for Olstein, he recalls that nobody liked J.C. Penney either when he started buying it in 2002 at $20 a share. Four years later he'd quadrupled his investment.

Southwest Airlines (LUV)

It has been quite a year for airline stocks. American Airlines shares are up 26 percent; US Airways, 33 percent; and Continental Airlines, 70 percent. The exception, ironically, has been the carrier that makes the most money: Southwest Airlines. Despite a 25 percent increase in earnings, Southwest stock was down 3 percent as of early December. The cut-rate carrier now has a 2007 P/E ratio of 16, its lowest in years. Bottom line: It is an ideal time to buy one of the best-run companies and best-performing stocks of the past 30 years.

Explanations for why Southwest has fallen out of favor just don't hold up under scrutiny, according to Citigroup analyst Andrew Light. One concern is that the airport hassles and heightened security measures that dented third-quarter earnings - a byproduct of the British airline terror plot - will extend into 2007. The reality is that things are pretty much back to normal, as evidenced by the 12 percent rise in Southwest's revenue passenger miles (a key airline metric) in both October and November.

Another worry is that Southwest's cost advantage is narrowing. In fact, Southwest's cost advantage over traditional carriers is still substantial. Thanks to superior hedging, Southwest will pay $1.54 a gallon for jet fuel in 2007, vs. $1.91 for American and JetBlue, Light estimates. Southwest's nonfuel costs are on average 30 percent lower than those of its major rivals.

Perhaps the biggest concern of all is that Southwest is now too big to keep growing at a high rate, an assertion that CEO Gary Kelly fiercely rejects. "Our growth opportunities are as strong in the near term as they've been in years," he says, pointing to new revenue sources such as cargo; new markets like Denver, Philadelphia and Fort Myers, Fla.; and the potential to capture routes, gates and passengers from competitors going through mergers or bankruptcies.

What's the endgame for Southwest? Morgan Stanley airline analyst William Greene envisions a future in which Southwest is able to increase its market share in the U.S. to a stunning 50 percent, from 17 percent today. "Southwest's low fares and leading cost structure would likely foster an environment where it would be difficult for carriers to justify significant capacity additions if their costs were substantially higher than Southwest's," Greene wrote in a recent report. "If we're right about the future of the U.S. airline industry, Southwest's profits and share price are likely going much, much higher." Nothing wrong with up, up and away.

Quelle: CNN.com

__________________

liebe Grüße von Coco

|

|

|

|

|

03-01-2007, 14:49

|

#3

|

|

TBB Family

Registriert seit: Apr 2002

Beiträge: 13.479

|

Six top European stocks

The search for the next great eurostars

Europe's economies may be growing slowly, but its markets are heading for a fourth year of double-digit increases. We found six promising stocks

British Petroleum

NYSE: BP

Price: $69

52-week low: $63

52-week high: $77

P/E ratio: 10

Yield: 3.5%

For Britain's BP, 2006 has been what Queen Elizabeth II once called an annus horribilis. From a pipeline leak that forced the company to close its Prudhoe Bay oilfield in Alaska in the summer to billions in legal claims stemming from a disaster at a Texas refinery, the past 12 months have been an exercise in what analysts call "headline risk." But while those problems have been a major headache for CEO John Browne and have revealed deep management failures at BP's North American unit, the long-term outlook remains solid. The company is still the second largest of Big Oil's super-majors in terms of production (only Exxon Mobil is bigger), with huge untapped reserves stretching from Russia to West Africa to the Gulf of Mexico.

For investors there's a silver lining to BP's stormy year. Despite bumper profits from record oil prices, BP shares have underperformed rivals such as Exxon, Chevron and Royal Dutch Shell, making the British giant an appealing value proposition. While Exxon is trading at 11.8 times next year's earnings, BP carries a multiple of only 9.8. "At the end of the day, BP has reasonable growth prospects and no longer trades at a premium," says Putnam's Byrne. Meanwhile, BP's multibillion- dollar stock-buyback plan and its 3.5% dividend offer further downside protection. Even if oil prices moderate, says Bear Stearns analyst Nicole Decker, "BP is among the rare few companies that will continue to grow organically at a reasonable cost." Plus, says Decker, 2007 should see a recovery in both the company's image and its financial performance as it puts Alaska, Texas and other trouble spots behind it. She thinks BP shares could hit $82 by the end of 2007, a 21% gain over the current $68.

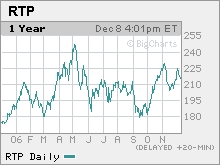

Rio Tinto

NYSE: RTP

Price: $214

52-week low: $171

52-week high: $253

P/E ratio: 11

Yield: 1.4%

Rising oil prices may have grabbed the spotlight in recent years, but they're only a small part of the global commodities boom. Metals have appreciated even faster. Copper has nearly tripled over the past year, as demand from China and other emerging markets has soared. Mining stocks have jumped as well, but few companies are better positioned to benefit than Britain's Rio Tinto. With huge operations in Australia (shares are listed in both London and Sydney), Africa and the Americas, Rio Tinto expects revenues this year to grow 25% compared with last year's, while profits should finish up more than 50%.

Copper and iron ore account for 75% of earnings, but the company also has valuable exposure to other hot metals, such as uranium. Even better, it has deep reserves, including an interest in four of the world's top ten undeveloped copper projects. Iron ore production is also growing rapidly, says J.P. Morgan analyst David George, which should help earnings even if copper prices cool off. And with a P/E ratio of ten and minimal debt, Rio Tinto is cheaper than such rivals as BHP Biliton, which trades at more than 12 times earnings. George sees a 30% upside in Rio Tinto shares, which have pulled back recently to $215 amid global fears of an economic slowdown.

Credit Suisse

NYSE: CS

Price: $68

52-week low: $50

52-week high: $69

P/E ratio: 12

Yield: 3.4%

Our next pick, Credit Suisse, is well known in the U.S. as a major player in investment banking, but back home in Switzerland, says Putnam's Byrne, it has long played second fiddle to UBS because of the latter's dominance in wealth management. Now that's changing: Credit Suisse sold its slow-growth insurance business, Winterthur, to AXA for $10 billion this summer and is focusing on its own wealth management business while boosting margins at its U.S. investment bank. The Zurich giant has also launched an aggressive stock-buyback program, with the goal of snapping up nearly $2 billion of its stock, or 3% of outstanding shares, by next April.

Like our energy-sector recommendations, Credit Suisse is also reasonably priced, trading at 10.9 times forward earnings, compared with P/E multiples of 12.6 for UBS and 11 to 12 times earnings for U.S. investment banks, according to Citigroup analyst Jeremy Sigee. In November, Sigee upped his rating on Credit Suisse from hold to buy, while increasing his target price to $75. With Credit Suisse currently trading at $67 - and boasting a 2.8% dividend - you're looking at a potential gain of nearly 15%. Not bad for a typically conservative Swiss bank.

Ba nco Santander

NYSE: STD

Price: $18

52-week low: $13

52-week high: $19

P/E ratio: 12

Yield: 2.5%

While Credit Suisse has been refocusing on its core business, Spain's Banco Santander has been riding an expansion wave that has made it the biggest bank in the eurozone. Earlier this year it acquired Britain's Abbey National, boosting an international profile that also includes such rapidly growing Latin American markets as Brazil, Mexico and Chile. In addition, Santander is thriving because of the boom in its home market, where economic growth over the past ten years has averaged 3.6% annually, nearly twice the rate of other European countries. Morgan Stanley analyst Pablo Beldarrain Santos, who rates Santander his top pick among Spain's banks, expects earnings to jump 25% this year and 20% in 2007.

Despite that kind of earnings growth, Santander remains reasonably priced, trading at ten times projected 2007 earnings, a 10% discount to other banks in Europe. If all that weren't enough, Santander pays a 3% dividend, which analysts expect to rise as profits grow in the next few years. Santos sees an upside of 20% in the shares of this fast-growing bank, which are now trading at $18 for its U.S.-listed ADRs.

Veolia

NYSE: VE

Price: $67

52-week low: $43

52-week high: $68

P/E ratio: 29

Yield: 1.4%

Although Veolia has been in business in France for more than 150 years, its name may be unfamiliar even to investors who follow European business. Formerly the water-supply and environmental- services division of Vivendi, Veolia was split off and renamed in 2003. Since the split from the entertainment side of the business (which retains the Vivendi name), Veolia has thrived, nearly doubling over the past two years on strong growth in its utility business in France and around the world. In the U.S., for example, Veolia supplies drinking water in Indianapolis and wastewater treatment at Kentucky's Fort Knox. Earnings growth for 2006 is expected to top 30%, while revenues are rising at a 20% rate.

For long-term investors, the appeal of Veolia is that it's a great way to play the growing demand for a commodity that in many parts of the world is scarcer than oil - fresh drinking water. In India, China and other emerging markets, population growth and environmental pressures offer Veolia tremendous opportunities in areas like water treatment and desalinization. The company already provides water to nearly 19 million people in China and has also won new contracts recently in the Persian Gulf and in Yerevan, the capital of Armenia. Shares of Veolia have rallied since the summer, when management abandoned plans to merge with French construction company Vinci, but HSBC analyst Verity Mitchell still sees 20% upside in the stock, which currently trades at $66.

Royal Philips Electronics

NYSE: PHG

Price: $37

52-week low: $27

52-week high: $38

P/E ratio: 7

Yield: 1.2%

Our last pick, Royal Philips Electronics, is well known as a maker of consumer products like Norelco shavers, light bulbs (the British royal family recently asked Philips to light Buckingham Palace with its low-energy bulbs) and medical devices such as CT scanners. But on Wall Street, says Franklin's Brugere, analysts have tended to focus on the company's huge but low-margin semiconductor business.

Now in the midst of a turnaround, Philips agreed in August to sell 80% of the chip business to private-equity buyers for more than $10 billion, freeing up cash for higher-margin divisions such as medical devices, as well as an aggressive stock-buyback program. With this transaction, says Brugere, "volatility has been reduced, multiple expansion is taking place, and management is doing what it has promised in terms of restructuring." Wall Street has taken notice: Philips shares have rallied since the August deal, rising from $30 to more than $37, and the company has boosted its multiple to roughly 22 times 2007 earnings. Even so, says Brugere, there's still an upside of 20% as this Dutch giant cuts costs, drives shareholder returns, reallocates capital, and earns new respect from the Street.

Quelle: CNN.com

__________________

liebe Grüße von Coco

|

|

|

|

Forumregeln

Forumregeln

|

Es ist Ihnen nicht erlaubt, neue Themen zu verfassen.

Es ist Ihnen nicht erlaubt, auf Beiträge zu antworten.

Es ist Ihnen nicht erlaubt, Anhänge hochzuladen.

Es ist Ihnen nicht erlaubt, Ihre Beiträge zu bearbeiten.

HTML-Code ist aus.

|

|

|

Es ist jetzt 06:51 Uhr.

|